How to Reduce the Surprise Factor in Retirement Planning

It takes a lot of planning to design a successful retirement strategy. Working with your clients to ensure that they are saving and investing enough to fund a comfortable retirement is critical, but there are other things to consider as well. Lifestyle, medical expenses, pension and Social Security, and charitable giving are all pieces of the retirement puzzle.

One aspect of retirement planning that your clients may overlook is tax planning. Taxes can have a real effect on retirement, and not planning for them can cause big surprises. Here are some common tax surprises that retirees come across, and what you can do to help your clients avoid them.

Retirement Plan Distributions

One of the biggest tax surprises for retirees who have saved diligently for the future by contributing savings to 401(k)s, IRAs, or other retirement plans is the tax that is due when they withdraw money from “pre-tax” plans. The tax that was deferred during their working years is now due when they withdraw money from the accounts – and many retirees are not prepared for this. If your client relies on “pre-tax” retirement accounts as a main source of income early in retirement, they may find themselves in a high tax bracket. This can get painful if their only way to pay the taxes on the distributions is by taking even more from them. Educating your clients on what they will pay taxes on in retirement is a critical part of a successful retirement plan, but there are also ways to achieve philanthropic goals and alleviate some of the tax burden.

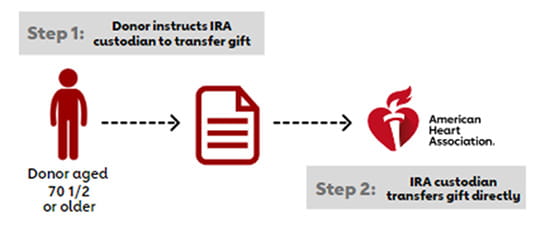

If your clients have philanthropic aspirations, there are strategic ways to alleviate some of their tax burdens while helping them achieve their charitable giving goals. Qualified charitable distributions (QCDs) can often be the most tax-efficient way to make a donation. Qualified charitable distributions are transfers from an IRA made directly to a qualified charitable organization without having this distribution counted as taxable income. Because funds go directly from an IRA to the chosen charity, this lowers the account owner’s adjusted gross income and effectively lowers their income taxes.

Clients 70 ½ and older can transfer up to $105,000 to charity tax-free each year (limit indexed for inflation annually). For clients 73 and older, the transfer may count toward their required minimum distribution (RMD) for the year.

Qualified charitable distributions also offer other avenues for supplemental retirement income. Effective January 1, 2023, the Legacy IRA Act expanded the definition of qualified charitable distributions to allow IRA owners to make a one-time distribution of up to $53,000 (indexed for inflation annually) to fund a charitable gift annuity or charitable remainder trust, which may then generate dependable income for the rest of your client’s lifetime.

Social Security

Tax on Social Security benefits is another tax component that your clients should be made aware of. Social Security benefits in retirement may be partially taxable, mostly taxable, or not taxable at all. It depends on your client’s “combined income” for the year. For a couple filing taxes jointly, neither of their benefits are taxable if their combined income is less than $32,000. 50% of the benefits are taxable if income is between $32,000 and $44,000, and 85% of the benefits are taxable if income is more than $44,000. As you can see, an increase of just a few thousand dollars in income can cause an unexpected increase in your client’s taxes in retirement.

Capital Gains

Capital gains tax can cause surprises for your clients with investments. Selling investments for retirement income rather than distributing from retirement accounts can provide real benefits for your client. However, selling investments can cause taxes, and qualified dividends and long-term (more than one year) capital gains are taxed at a 15-20% tax rate — or even 0%, depending on your client’s income. Capital gains can really add up if enough investments are sold during the year; combined with other sources of income, your client could end up with higher tax rates on those gains, reducing the tax advantage.

Once again, turning toward charitable giving is a strategic way for your clients to escape capital gains tax while creating a legacy. One of the most tax-savvy ways to give is through a donor advised fund (DAF). Instead of giving directly to charity, your client can establish a donor advised fund with an irrevocable gift – which could include cash, stock, real estate and more. Those funds can then be invested for tax-free growth, and your client can suggest how the money should be distributed to the charities they support either now or in the future. Your client claims a deduction for the year in which they fund the account – even if they wait until future years to ask the fund to make grants. Donating appreciated securities to the donor advised fund gives your client the added benefit of avoiding capital gain taxes on the sale of the securities, since the fund can sell them with no tax.

Medicare Premium Surcharges

Medicare is the primary health insurance for millions of retirees aged 65 and over. Original Medicare (parts A and B) covers most hospital and medical costs. Other parts of Medicare (Part C, Part D, and Medigap) are private insurance plans that provide additional coverage. Part A has no premium, but all the other parts involve a premium.

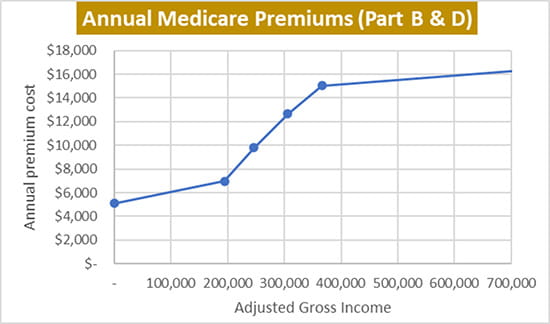

The basic Part B premium is $164.90 per month for 2023. However, added premium surcharges called income-related monthly adjustment amounts (IRMAA) can more than double your client's Part B and Part D premiums. IRMAA surcharges are based on an individual’s total income, so while they are not technically a tax, they act like a tax. For instance, a couple filing a joint tax return with income under $194,000 will typically have Part B and Part D premiums of about $5,000 for the year. However, if their income is over $194,000, IRMAA surcharges can raise their total premiums to over $16,000 a year.

How to Reduce the Surprise Factor

Having less tax surprises in retirement means helping your clients plan for retirement well in advance. This means planning for which accounts to draw from, and which pension, Social Security and Medicare options to choose. It also means being careful about tax-generating activities like retirement plan distributions and capital gains. Achieving an understanding of both your client’s financial and philanthropic goals can be a strategic way to help alleviate some of their retirement tax burdens while simultaneously making an impact on the causes they care

deeply about.

About the Author

Jon Beyrer, CFP®

Senior Financial Advisor, Blankinship & Foster, LLC

Jon P. Beyrer, CFP®, EA® is a Certified Financial Planner practitioner and is a principal of Blankinship & Foster LLC, a nationally recognized wealth advisory firm in Solana Beach, California. Jon has been providing personal financial advice and guidance to families and individuals since 2001. As a lead advisor, he focuses on helping families achieve their goals by integrating sound wealth planning with investment and tax planning.

Jon earned his Master of Science Degree in Financial and Tax Planning in 2001 from San Diego State University and his Bachelor of Science Degree in Finance in 1995 from San Diego State University. He is licensed to use the Certified Financial Planner® and CFP® marks by the Certified Financial Planner Board of Standards and is enrolled to practice before the IRS.